Keep calm, and remember: Volatility is a natural part of long-term investing

First National Wealth ManagementApril 8, 2025

Fear and uncertainty surrounding the federal government’s tariff policies are causing enhanced stock market volatility.

The S&P 500 Index of U.S. stocks is down 14% year-to-date as of April 8 (though still up 35% since January 1, 2023).

It might not feel this way, but the type of decline we are experiencing today is quite normal, historically speaking.

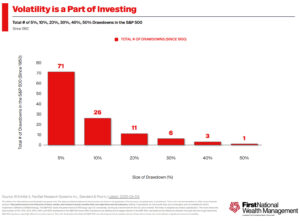

In fact, the chart below shows that we have experienced 26 10–20% drawdowns since 1950, or about one every two to three years.

Each time, the cause of the decline was unique and painful to live through.

However, in all prior cases, the market has gone on to fully recover and reach new highs. The facts may have been different, but the story remained the same.

If you own bonds and cash, they are doing their job of providing stability and income.

Though we don’t know how long the current malaise will last, we are confident the market will fully recover and reach new highs in the future.

Should I be doing something about stock market volatility?

You might be wondering if you should be doing something in response to the market declines.

Should you sell stocks now and buy back later?

While it may sound appealing, it is basically impossible to time the markets in practice, and it introduces significant risk to meeting your long-term goals.

Instead, we recommend thinking of stock market volatility as a fee we must pay to earn the 10% return stocks have delivered over the course of the last century, rather than a fine to be avoided.

In the below passage originally published on Collaborative Fund’s blog (2019), famed finance writer Morgan Housel explains the difference between fees and fines as it relates to volatility.

“Question: Is that volatility a fee or a fine?

Fees are something you pay for admission to get something worthwhile in return.

Fines are punishment for doing something wrong.

It sounds trivial, but thinking of volatility/drawdowns/uncertainty/pain/terror/ulcers as fees instead of fines is an important part of developing the kind of mindset that lets you stick around long enough for compounding to work.

Few investors have the disposition to say, “I’m actually fine if I lose 20% or more of my money.” This is doubly true for new investors who haven’t experienced a 20% decline.

But a reason declines hurt and scare so many investors off is because they think of them as fines. You’re not supposed to get fined. You’re supposed to make decisions that preempt and avoid fines. Traffic fines and IRS fines mean you did something wrong and deserve to be punished. The natural response for anyone who watches their wealth decline and views that drop as a fine is to avoid future fines. But if you view volatility as a fee, things look different.

Disneyland tickets cost $100. But you get an awesome day with your kids you’ll never forget. Last year more than 18 million people thought that fee was worth paying. Few felt the $100 paid was a punishment or a fine. The worthwhile tradeoff of fees is obvious when it’s clear you’re paying one.

Same with investing, where volatility is almost always a fee, not a fine.

Returns are never free. They demand you pay a price, like any other product. And since market returns can be not just great but sensational over time, the fee is high. Declines, crashes, panics, manias, recessions, depressions. You’re not forced to pay this fee, just like you’re not forced to go to Disneyland. You can take them to the local county fair where tickets might be $10. You might still have a good time. But you’ll usually get what you pay for. Same with markets. The volatility/uncertainty fee is the cost of admission to get returns greater than low-fee parks like cash.

The trick is convincing yourself that the fee is worth it. That, I think, is the only way to deal with volatility; not just putting up with it, but realizing that it’s an admission fee worth paying.

There’s no guarantee that it will be. Sometimes it rains at Disneyland.

But if you view the admission fee as a fine, you’ll never enjoy the magic.”

Controlling what we can control

You can trust that here at First National Wealth Management, we are focused on controlling what we can control.

We are proactively monitoring your cash balances to make sure we have enough on hand for anything we know you will need in the near future.

We are monitoring your portfolio and rebalancing your investments to be in line with your pre-established mix between stocks, bonds, and cash.

We always manage your money assuming that challenging times will come.

It is embedded in our investment philosophy and in the financial planning work we do with many of you.

We remain disciplined and unemotional, ready to take advantage of any major opportunities that may come our way.

Please feel free to reach out to us with any questions or concerns. We are here for you.